My annual confession on the road to 10X every 10 years

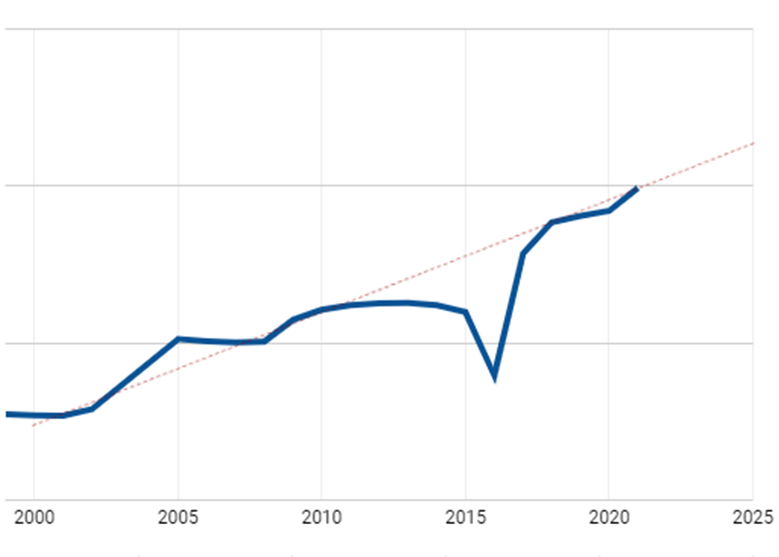

I committed to holding myself publicly accountable to my RE (real estate) goals which is to 10X my portfolio every 10 years. This is my annual update, my back story, and my previous self-review. The chart shows my real estate investment holdings on a log y-axis (each horizontal line is 10X the one underneath):

Annual update (2021)

COVID-19 was a year long test. It reminded me of 2008. A test to see if I held my conviction about real estate investing in the face of uncertainty. If I radically changed my mind I wouldn't be investing, I'd be speculating. But as most of us probably felt, nervousness was in the air around June/July last year. I made five good real estate decisions during the last twelve months, one bad one, and had one near miss.

Good decisions

- I bought a quality 3-unit turnkey place with 5% cash-on-cash yield and 13% return-on-equity (before price appreciation and any depreciation benefits). I wrote about it here:

Laziest Landlord

Laziest Landlord

2. I am closing on another 3-unit place with 19%(!) cash-on-cash yield and 24% ROE. There were two owners (real estate brokers no less) that had fallen out professionally. They wanted to be shot of their partnership. I made an at-market-price offer within 24 hours of listing for this property with an accompanying pre-approved financing letter. (And I vigorously thanked my broker to alerting me to the opportunity!). Personal lesson: be ready to move fast on mispriced assets. They don't come around often.

3. I refinanced two properties when rates were rock bottom. I refinanced one commercial loan from 3.59% to 2.52% while keeping the amortization length. Personal lesson: don't try and time any market perfectly. Take chips off the table.

4. I decided to build bank relationships before finding investment opportunities. I now have a roster of about seven solid lenders who know me and my investment goals reasonably well. One commercial loan I secured 25% down, 10 year fixed, 35 year amortization at 3.25%. Personal lesson: relationships matter, particularly when it comes to commercial lending. I wrote about it here:

Laziest Landlord

5. I made the most of cheap refurbishment costs at the height of the pandemic. In May 2020 I contracted a full gut job on one of the apartments I own. Floors, walls, bathrooms, appliances, you name it. The total cost was under $30K for the middle of Toronto. I put rents up ~12% and locked in before the Toronto rental market tanked. Personal lesson: make the most of 'temporary dislocations' in the market.

Bad decisions

I was about to buy a 3-unit in the middle of Toronto in June 2020. I didn't. I made a classic mistake and did a mental 'worst case' scenario. It's an amazing location and the price was a steal. It needed refurbishing which I could have done cheaply at the time. Personal lesson: do "75/25" assessments...what's the likely outcome at the 75th percentile chance and the 25th percentile chance.

Near misses

Another mispriced asset: this time the offspring of a wealthy UK resident wanted to offload three units in an eight unit townhouse in Boston. The three units together were about 15% under market value. There was a legal tussle with the condo board that wanted to acquire part of the basement unit common area from one of the properties. That space was probably worth $100K as a laundry room or storage facility. I recognized this space as additional upside. Four lawyer groups ended up involved. I couldn't get to speak directly to the seller. Unsurprisingly the deal died. I don't consider it the worst loss. Personal lesson: work around lawyers quickly in the process.

Overall, I consider 2020/21 a good 12 months in my real estate adventures.

The back story

My goal is to 10X my real estate investment value every 10(ish) years. I will do this by buying one three-to-six unit building every two years and renovate each unit every ten years. I use a combination of cashflow from existing properties, tax write-offs, personal income, and refinancing.

I started with £10K at the turn of the millennium. Back then I was in England selling chocolate and earning a little over £20K (roughly $30K). I used to drive my car no faster than 60 mph because I knew it would save me pennies worth of fuel. The place across the street did burger, fries, a beer and an hour of pool for five pounds on Sundays. I knew how to stretch my money. I still do.

I bought my first two bedroom apartment in Leeds, UK knowing one day I'd rent it out. It overlooked the canal (big plus). It had addicts injecting outside my living room window (big minus).

My down payment was about £10K. My mortgage rate was nearly 6%. I cut back on my groceries because of the principal and the interest payments.

I fixed the place up myself. I re-tiled the bathroom, installed new lights, and installed a new radiator. I repainted the kitchen cupboards. I didn't know how to do any of this. I read books, got friends to show me, and just tried. I nearly electrocuted myself getting the positive and negative wires wrong on an overhead light fixture. I can still grout. I still hate it.

You have to start somewhere. "The faster you buy your first home, in my opinion, the better...You’ve got to get in the game.” ~ Barbara Corcoran

I moved out and moved abroad four years later. I rented out my Leeds apartment fully furnished. The rental income covered the costs of the unit and most of my room rent in Canada. I sold the place and realized a 30% gain in property value. It was a 5X gain on my original investment. I now understood leverage and ROI.

That was the start of knowing I could make real estate work. I learned a few "don't's" on that first property.

- Don't renovate yourself unless you're fast and capable or have no other options. A $30 per hour contractor [update: this seems an impossible number today!] is a deductible expense. If you work at a third of his or her speed, you're saving $10 per hour. Once you factor in taxes, maybe $6 per hour. Not worth it.

- Don't lease furnished places yourself unless you're prepared to invest a lot of time. Furniture and decor gets banged up quickly. Small items need replacing. Tenants expect more 'service'. Large items need disassembling and junking. The ROI on the furnishings is great (about 25% by my estimates). The time and energy investment on furnishings is dreadful.

- Don't compromise on the contract. Penalize late rental payments and damages (where local laws allow you to). Be tough in the contract so you don't need to be tough later on.

- Don't compromise on tenants. Dirtiness. Noisiness. Carelessness. Tardiness. All cost you in repairs, hassle, or cashflow. Better to get a great, considerate tenant for $100 less a month than a bad tenant. Losing a months' rent because a place needs fixing up or isn't ready to show is a real loss.

- Don't be disorganized in your paperwork. Scan and file everything. You will need access to almost every paper at some point. Disorganized now = time wasted later.

Every landlord has a myriad of horror stories. I'm no different. Every one of these five lessons has more than one story behind it. You can learn them from me, or you can learn them yourself. I've had zero bad experiences in the last ten years. Zero.

Annual update (2020)

In 2020 I've evaluated (run the Excel model for) approximately 50 potential rental buildings. Most are in the Greater Boston area. All have between three and six units. Some have commercial spaces. I've visited about ten of those. And I've made three (unsuccessful) offers.

Cap rates are probably 1% lower in the same Boston areas than they were last year. My guess is two things are driving down cap rates.

- Mortgage interest rates are about 0.75% lower than last year. Costs (interest payments) are lower for investors using financing. Investors looking for cashflow are, therefore, willing to take a lower cap rate.

- Investors are looking for investment stability. The stock market has been a wild ride this year (so far). Real estate investors might be willing to pay for that stability. Again, that willingness might show up in lower cap rates.

(Cap rates 101):

Laziest Landlord

I've started considering towns just outside Boston, like Medford, MA. Many downtown Boston offices have been closed because of COVID-19. I think there will be a permanent shift of a small population of professionals who work a few days in the office and a few at home. I expect they will move along commuter rail routes looking for more personal space. But I think the downtown core of Boston - Back Bay, Southie, the North End etc. - will continue to be popular with young professionals for the nightlife. I expect to find a three or four unit place which meets my investment criteria by the end of the year. But I'm in no rush. I get more dispassionate every year.

I've also looked for apartments in the downtown core of Toronto. The returns compared to Boston are horrible. In Boston I aim for a 12% ROI and 6% positive cashflow with 20% down (25% at a stretch). In Toronto in 2020 I have yet to find a single cashflow positive place for a similar percentage down. I've evaluated perhaps 10 units of all sizes - from bachelors to three bedroom apartments. My hypothesis is that there's a enough international (primarily Chinese) investment dollars looking for a safe haven. Returns are less important than capital preservation for these investors. Trump is restricting highly skilled immigrant visas to the US. Canada - and by extension Toronto - is a solid alternative for those immigrants. I'm unclear about the future economics in Toronto. But I expect demand to hold.

During COVID-19 I'm taking the opportunity to renovate one unit. Contractors and materials are cheap. I got a 15% discount to normal rates (a gut job renovation for $30K in Toronto, including floors, appliances, two bathrooms). I expect rents to increase by around $300 per month. The payback isn't great. But it's a necessary expense and the first meaningful outlay I've had in 12 years. I budget 0.3% of annual rental value as repairs. This is right on target.

The last four unit (12 bedroom) place I bought in 2018. It has such strong cashflow I was able to refinance down from a 30 year fixed mortgage at 5.25% to a 15 year at 3.5%. This is the exact reason I love real estate investing. Rents have risen. My costs have come down. My insurance broker found insurance 40% cheaper this year. There was no change in coverage.

COVID-19 has not hurt rent collection for 2020 so far. Normally my places are all rented by June for a September 1 start. 3 units remain not rented. The next 4-6 weeks will be telling. Ultimately I've got room to reduce rents by $150 per room per month to avoid vacancy.

This is the riskiest investment market I've seen since 2008/09. Interest rates are not the issue. Tenant behavior and solvency is. If young professionals decide to rent in different neighborhoods that will put pressure on my rents. If young professionals get laid off or furloughed without government support that will put pressure on my cashflow. If fewer students come in person to Boston there will be higher vacancy across the city.

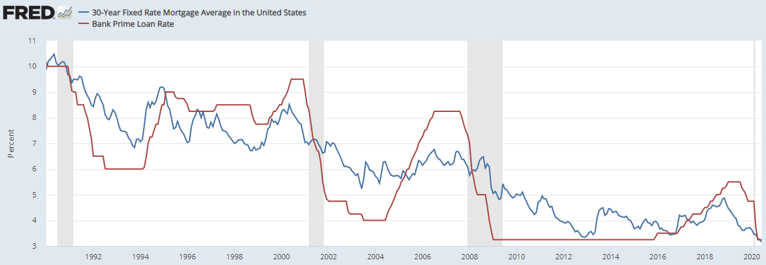

The flipside of this risky market is mortgage rates may come down further. By how much, if at all, is unclear. The Federal Reserve Bank of St. Louis shows some periods where 30 year fixed rate mortgages are lower than bank prime.

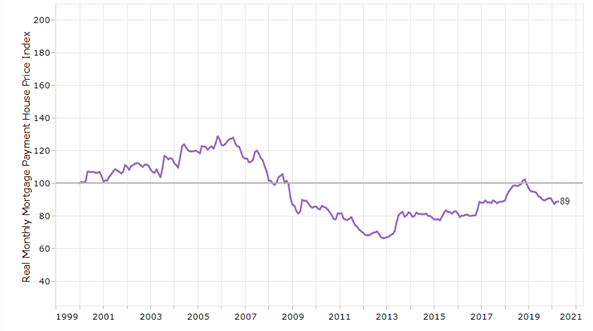

Prices in Boston are fairly moderate using inflation- and rate-adjusted Case-Shiller. This data gives me confidence in the local market in the mid-term.

Conclusion for back half of 2020: I'm going to continue to invest in the Greater Boston area. I'll be more aggressive on a lower purchase price to balance some of the market risks. I'm only looking at multi-family units. None have storefronts.