Make more money whether interest rates go up or down

If interest rates go up, don't refinance. If interest rates go down, refinance.

(Refinance means, in this case, 'replace your current loan with a new loan').

I have no idea what interest rates are going to do. Neither do you. That's the truth. But changes in interest rates are scary. Higher interest rates usually means inflation. Inflation eats away at wealth. Lower interest rates means the economy is growing slowly.

Here's what I do know. If you've financed your real estate investment with a fixed rate mortgage you have a 'heads I win, tails you lose' situation.

Say you put 35% down payment to finance a property at 4% interest rate with a 30 year mortgage . If interest rates go up to 6%, do you refinance? No! But you raise rent on your tenants. If rates go down to 3%, do you refinance? Yes!

Either way you win.

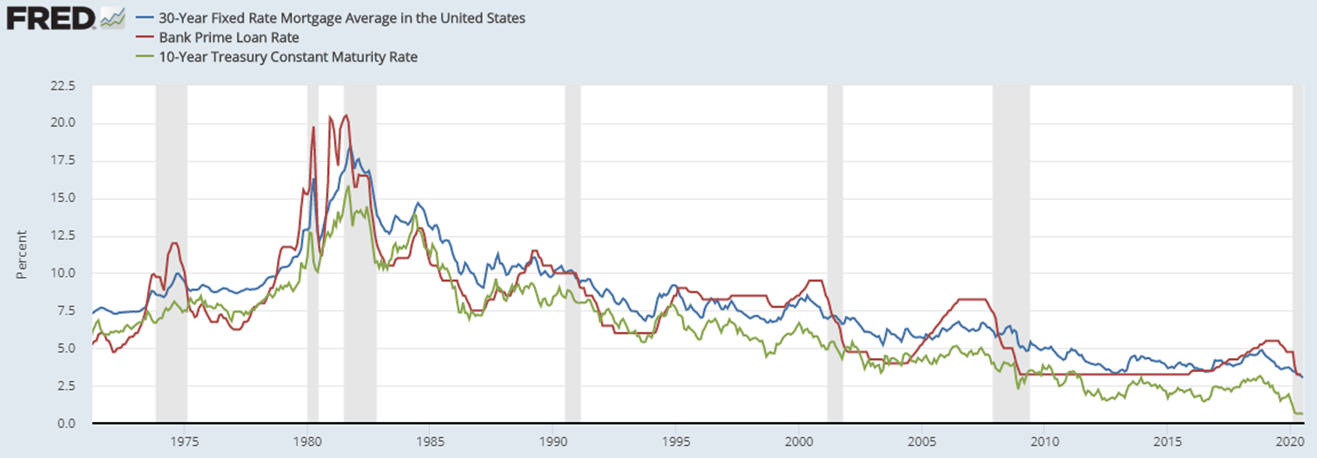

Mortgage interest rates follow the 10-year US treasury rate closely.

Source: Federal Reserve Bank of St. Louis

If 10-year US treasury rates rise, so will the cost of getting a new mortgage. If the same treasury rate falls, so will the cost of getting a new mortgage.

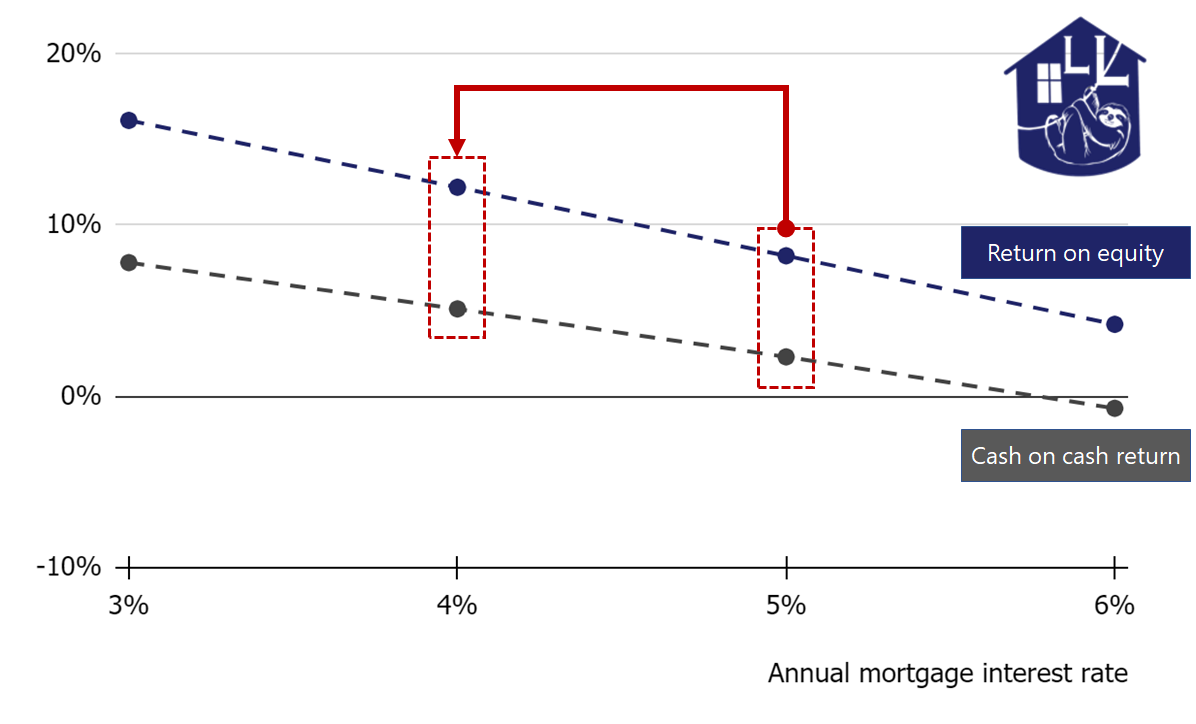

Here's a real example of a real property. If you put 20% as down payment at 5% interest rate, the return on equity (ROE) is 8.2% and cash-on-cash return (COC) is 2.3% in year 1. Let's say interest rates fall dramatically so you can refinance at 4%. ROE is now 12.2% and COC is 5.1%. That's a big improvement in financials.

ROE and COC with 20% down

Note: this analysis does not included refinance costs, or the ability to refinance with a bank. For simplicity it looks at year 1 data only.

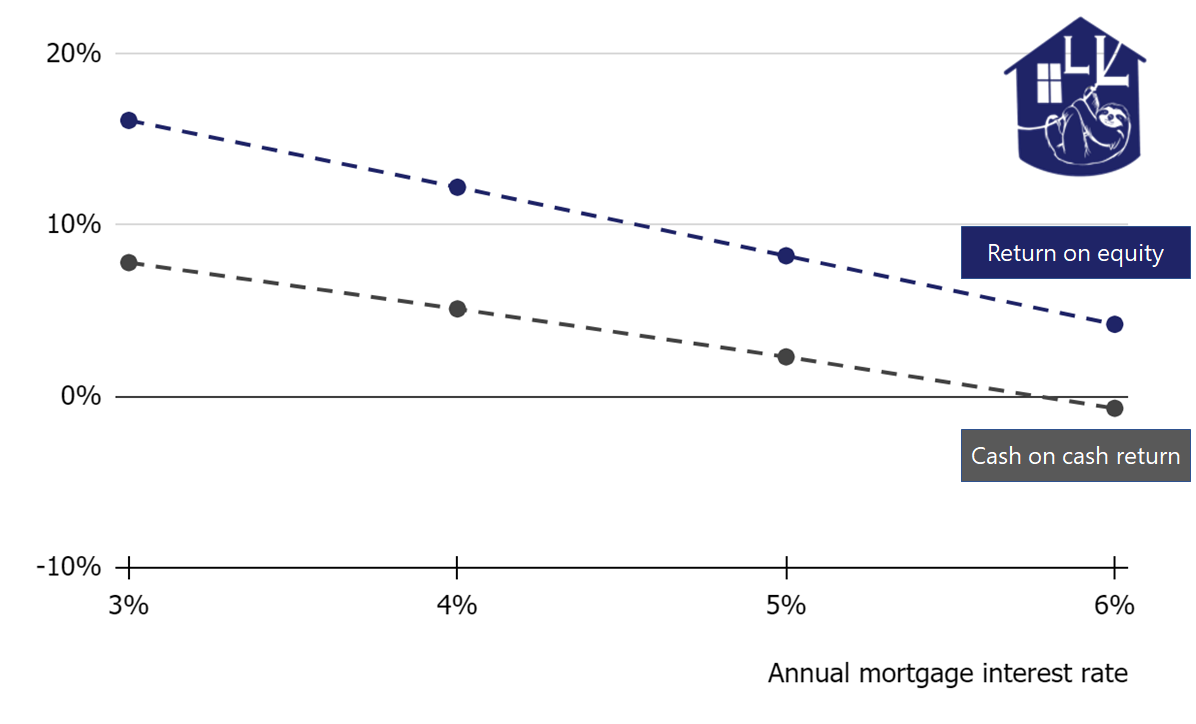

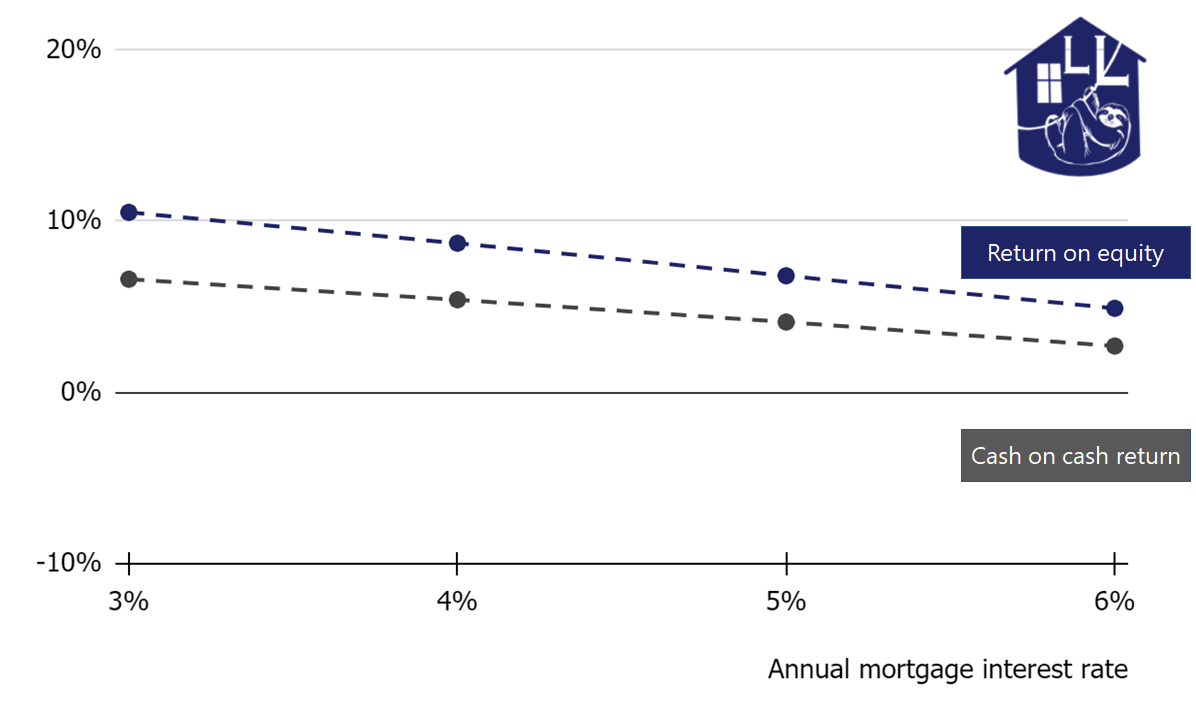

Let's take a brief diversion here. If you have a higher down payment, say 35%, then ROE and COC do not change as much if you refinance to a different interest rates. This is because fewer of the total dollars are borrowed and so fewer dollar are working for you. Compare the slope of the lines in the two charts below:

ROE and COC with 20% down

ROE and COC with 35% down

Refinancing at a lower interest rate is more powerful when your loan-to-value ratio is high.

Now let's say you have the same property with 20% as down payment (not 35%) at 4% interest rate. Recall the ROE is 12.2% and COC is 5.1%. Let's say interest rates jump up to 6%. You don't refinance. But you do increase rents by 2%. Then in this example ROE becomes 12.8% and COC 5.7%. Again, better financials.

(To make the numbers comparable, I've assumed this all happens in the same year and with utilities, property tax, insurance also rising by 2%).

If interest rates go up, increase your rents. If interest rates go down, refinance your loan. Leverage - or a high loan-to-value - magnifies the effect.

Never worry about the coinflip of interest rates again. Whether interest rates go up or interest rates do down, you win.