Rates banks don't advertise

If you're looking for a mortgage for your primary residence, banks compete hard. They know it's a commodity business. The rates are advertised everywhere.

But what about investment properties?

Banks charge a higher rate because you have less skin in the game. You're more likely to default on an investment property that you don't live in than your primary residence. And they don't advertise them.

I've spent time this week calling a myriad of banks. And I'll share what I've found.

First a few caveats.

- If you put your property in an LLC (I'll write a separate post on this) banks usually charge ~0.5% above a regular mortgage rate. Take it as a rule of thumb.

- For a commercial mortgage the terms are differently structured. For simplicity think of residential mortgages as a multifamily with 1 to 4 units and commercial as a multifamily with 5+ units or anything that contains retail/office etc. space.

- Residential rates are based on you, your credit, your debt-to-income ratio etc. They're pretty inflexible. Commercial rates are based on the property and something called Debt Service Coverage Ratio (DSCR). Terms are more negotiable (flexible) than residential rates.

- The rates are for the Boston area, for last week. They will change. They will be different where you are. They will depend on the property.

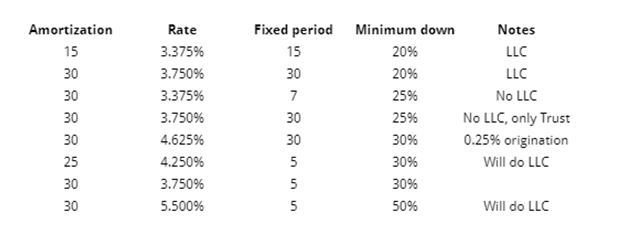

Investment property residential mortgage rates

You can see some banks won't fix the rate for more than 5 or 7 years, particularly within an LLC. There's a big gap between the best and worst rates in the table above. And in the down payment percentage. The rate and the down payment have a big impact on your cash flow and ROI.

One mortgage loan officer I spoke to said "we don't really want to do mortgages at the moment, so we make the rate prohibitively high".

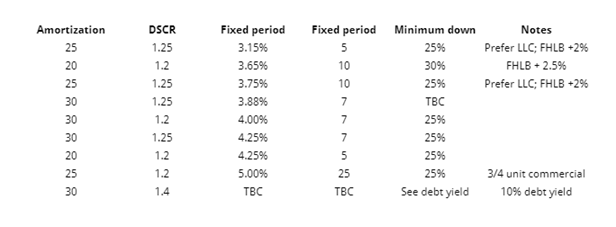

Investment property commercial mortgage rates

Commercial rates are rarely fixed for more than 10 years. Typical terms are 5, 7 & 10 years. The rates are often floating and priced off the 11 Federal Home Loan Banks (https://fhlbanks.com/about-us/) plus a premium. The terms above are the 'opening offers' for the banks. They're negotiable and would not be the final terms to close on.

How do you calculate DCSR? Take your Net Operating Income (NOI) and divide it by how much cash - principal and interest - you give the bank. It's the banks' way of making sure you have a cash buffer. DSCR is calculated on the basis of an annual P&L (or a proforma).

So now you know what kinds of rates you can expect. There are other ways of financing, such as private money. But the vast majority of Laziest Landlords will work with a bank. Call them before you make an offer.