COVID-19 is changing real estate investing...permanently?

I don't usually write about current trends. Real estate investing is - for me at least - a long term business. Decisions I make today have compounding benefits 5, 10, 20 years down the road. Nevertheless, the market is unusual and it is worth unpacking.

Let's take a look all the way from the long-term macro-trends down to the latest eviction ban. If you love charts and data, you'll love this post.

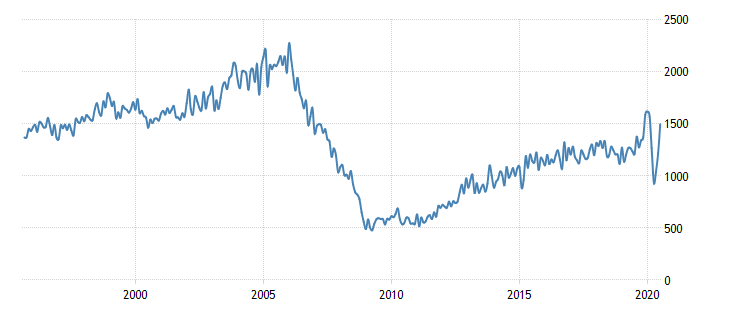

A. Renting nationally will sustain because we're still not building that many homes

US Housing Starts (000's)

Source: tradingeconomics.com; US census bureau (https://tradingeconomics.com/united-states/housing-starts)

We've just about reached the average annual builds back in the last 90's and early 00's. Supply nationally is constrained. That means there's not a lot of inventory going around.

B. Entry-level housing for young adults is being driven up by land prices

Share of Land Price in Home Value (2000 = Index of 1)

Source: Freddie Mac (http://www.freddiemac.com/fmac-resources/research/pdf/201707-Outlook-04.pdf)

(If you want to get really nerdy, water/mountains and growing populations constrain supply and drive up prices, see page 1277 and 1283.):

The tech boom has centered around coastal cities (constrained land). Younger people are hired disproportionately by the tech companies. Combine that with slower home building, and the result is entry-level housing prices going up and home ownership going down.

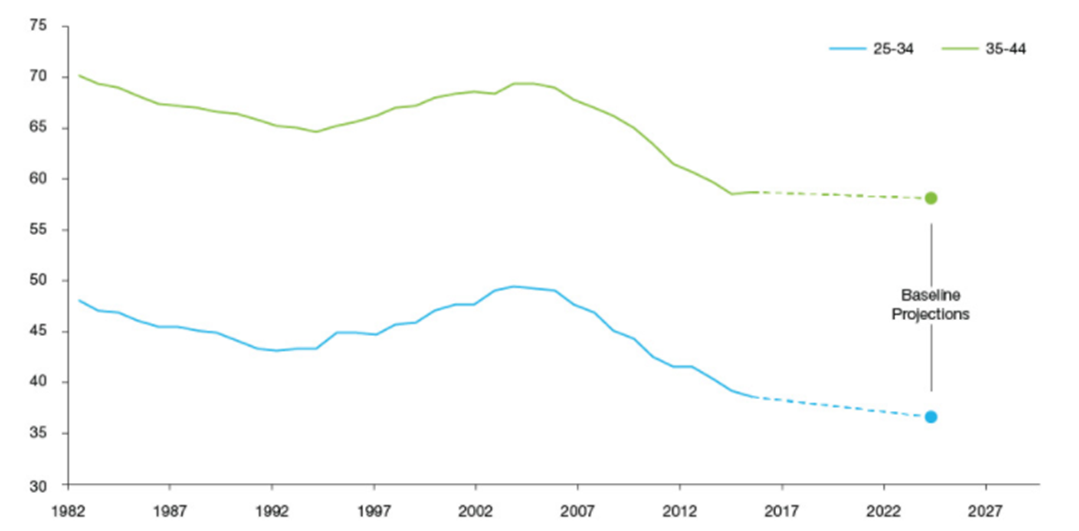

Home Ownership Rates by Age Group

Source: Freddie Mac; US Census Bureau (http://www.freddiemac.com/research/insight/20180628_rising_housing_costs.page)

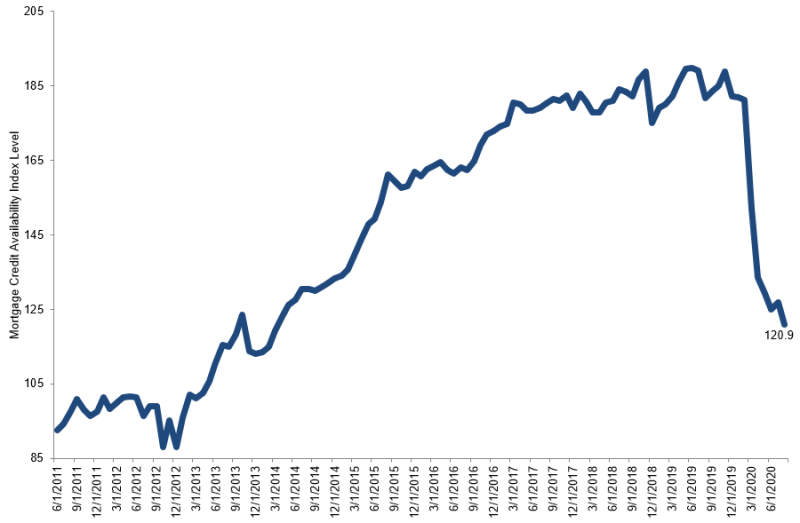

C. If you have good credit you're in a strong position to buy

US Mortgage Credit Availability Index (2012 = 100)

Source: Mortgage Bankers Association; Ellie Mae's AllRegs; Market Clarity (https://www.mba.org/2020-press-releases/september/mortgage-credit-availability-decreased-in-august); note a methodology change in ~2016

Credit has tightened. A lot. Lenders are going to take a very close look at your ability to cover investment properties. Anecdotally I've spoken to about ten lenders in the last six weeks and all of them have confirmed tightening lending standards. (As an aside, before the 2008 crisis this chart peaked at about 900. That's literally off the charts. You could get a mortgage if you had a pulse.)

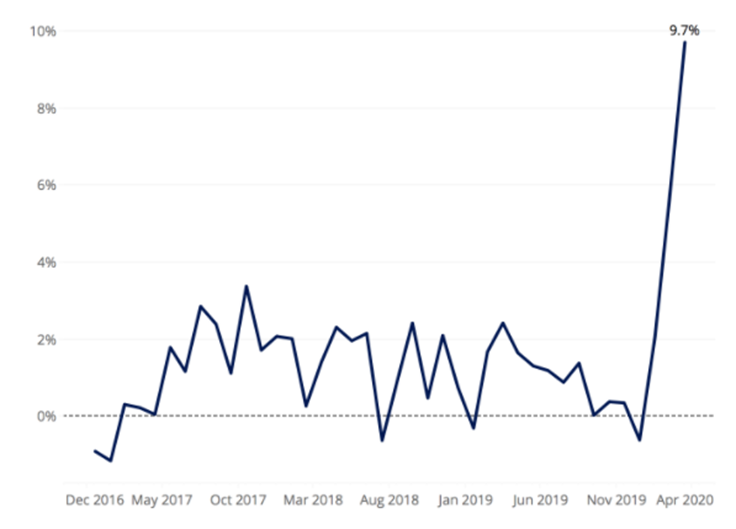

D. Lots of people moved out in summer (moved in with their families), but things have picked up in July & August

Annual Change Adults Living With Parent/Grandparent

Source: Zillow (https://www.zillow.com/research/coronavirus-adults-moving-home-27271/)

Move-ins as % of Move-outs YoY

Source: MRI real estate software (https://www.mrisoftware.com/resources/market-insights-report-covid-19-multifamily-august-2020/)

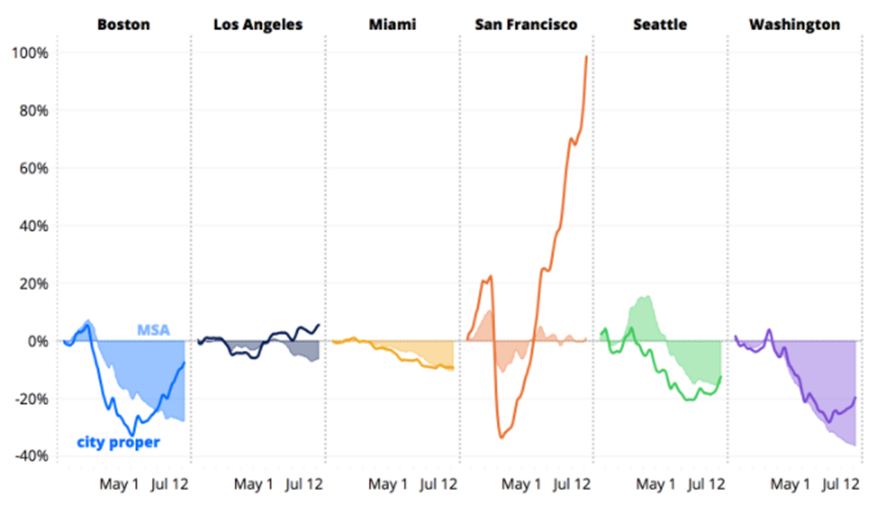

E. Where inventory is out of balance property prices will decrease - specifically San Francisco (and New York)

Change in YoY Inventory (since February 2020)

Source: Zillow (https://www.zillow.com/research/2020-urb-suburb-market-report-27712/)

Supply and demand are out of balance in San Francisco. Other markets look more balanced. For now at least.

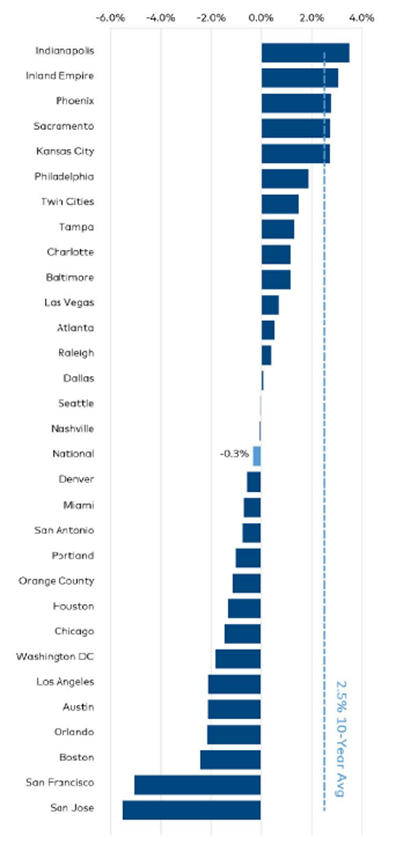

F. "Secondary" cities are great investment opportunities with rising rents in the short-term

YoY % Rent Growth

Source: Yardi (https://www.yardimatrix.com/publications/download/File/1069-MatrixMultifamilyNationalReport-Summer2020)

The tech cities - San Francisco, Boston, LA, Washington, Austin etc. - have all shown meaningful rent drops. Companies located in those cities have been more willing (and able) to let their workforce work remotely for an extend period of time since COVID-19.

Will this continue? Certainly well into next year. The next September renting season (2021) will be critical.

You can see how excess inventory in San Francisco shows up in lower rents.

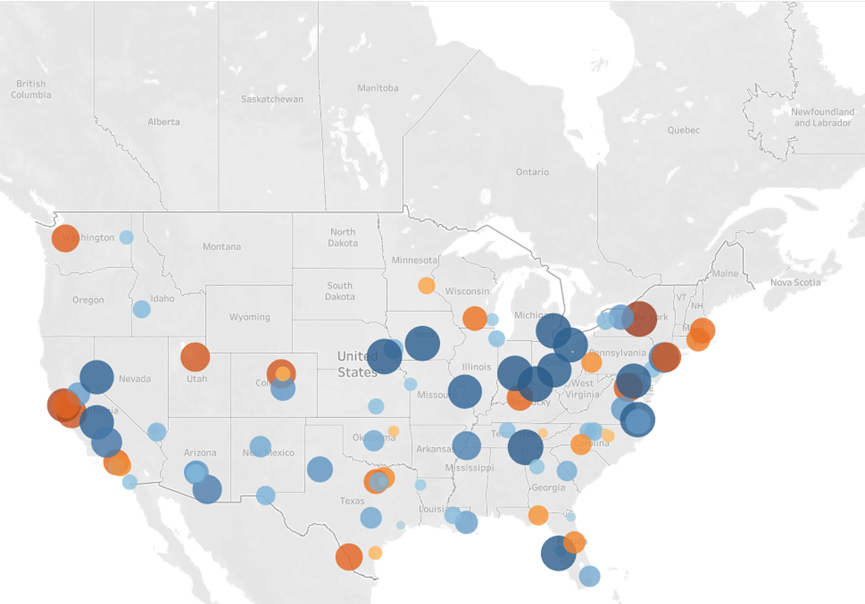

It's easier to see how people are moving from 'coastal tech hubs' to secondary cities:

1-bed Median Price Change YoY % (blue is positive, orange negative)

Source: Zumper (https://www.zumper.com/blog/rental-price-data/)

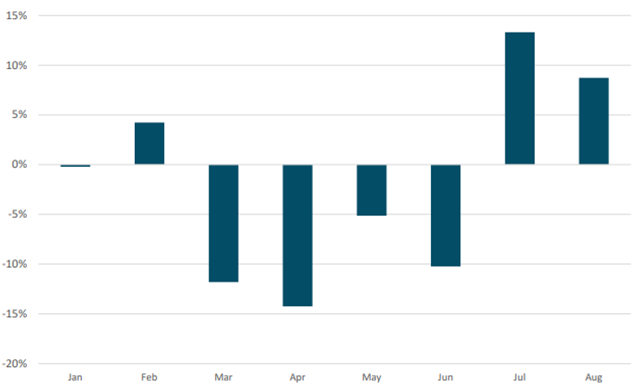

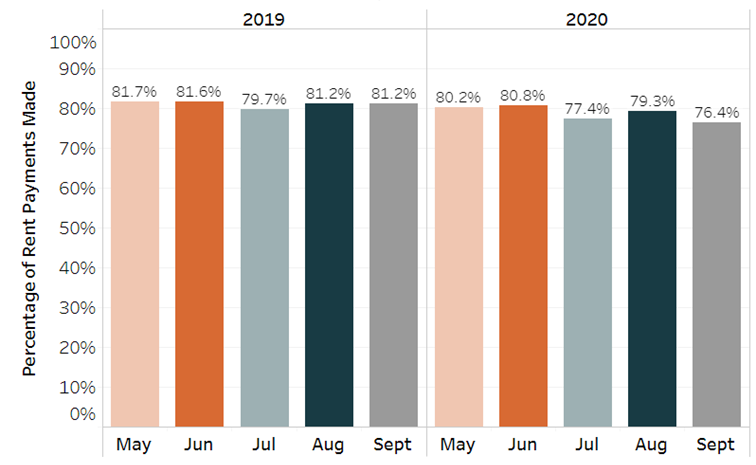

G. But some tenants are finding it harder to make rent since July

Weekly Rent Payment Tracker (~11M households, week ending 6th)

Source: National Multifamily Housing Council (https://www.nmhc.org/research-insight/nmhc-rent-payment-tracker/)

H. The new eviction moratorium is a kick in the stomach for landlords who are already down

The September 1 announcement by the CDC is bad for landlords. Landlords are small business owners (about eight to ten million of us in the US). I have immense sympathy for tenants who lose their jobs because of COVID-19 and need a roof over their heads. The CDC has declared some tenants cannot be evicted else landlords face substantial fines. But the CDC is putting 100% of the financial risk on landlords - small business owners - without due compensation. Property is an asset class. And assets need managing. Managing an asset through turbulent times like COVID-19 has been hard enough. The CDC just put the boot in. I support the CDC announcement if the federal government makes up 80% of the tenants' shortfall of rent. That way landlords are pitching in a meaningful contribution with everyone else.

CDC issues federal eviction moratorium through end of year

Who are the tenants that cannot be evicted? In short those who:

- Have used best efforts to obtain available government assistance for rent or housing

- Were eligible to receive a stimulus check under the CARES Act (or has restricted income)

- Are not able to pay the full rent because of lost income, hours, or high medical expenses

- Have been making best efforts to make partial rent payments

- Have no other available housing options

To reiterate: I understand the hardship for tenants. But the CDC announcement means landlords will understandably stay clear of buying the types of properties where tenants might not be evicted.

The question you're probably asking yourself is: "Are the changes in the rental market a blip or a trend?". I don't know. No-one does. What I do know is that dislocations like COVID-19 produce opportunities. The long-term outlook for being a landlord is good. Put simply: the US is building few homes. Affordability for young adults is hard. And right now getting a mortgage is difficult without good credit.

For me, real estate investing always has and always will be a long-term business. Here's how to play for the long-term while managing for the short-term:

Primary markets (San Francisco, Boston, LA, Washington, NY etc.): make sure a new real estate investment can support weaker rents and higher vacancy. Cash in on the rental upside if the demand rebounds in the next one to four years.

Secondary markets (Indianapolis, Sacramento, Tampa, Charlotte, Baltimore, Kansas City etc.): act soon to capitalize on rising rents and limited credit availability. Target properties and tenants where the CDC eviction moratorium is unlikely to be relevant. Plan for downside if renters move back to primary markets and rents soften.