Love paying tax? Then don't read this

Once you start real estate investing you realize all sorts of tax advantages. I am not suggesting you should invest in real estate because of the tax benefits. It's like getting a free dessert with your dinner at a restaurant. A welcome surprise that you will definitely want to eat.

Here's what's cooking.

If you're a truly lazy landlord, your property management fees are tax deductible

If you're paying someone to manage your property - which I recommend - the costs are expenses. Say you're paying 4% to your property management company and you're making a handsome profit on your rental. The effective cost to you is 4% x (1 - 32%) = 2.72% if you're in the 32% tax bracket.

You can deduct all sorts of other expenses by owning the property:

- Mortgage interest

- Repairs

- Utilities

- Property tax

- Advertising expenses (but your property manager should be doing this!)

- Landscaping

Trump's Tax Cuts & Jobs Act 2017 means you can also write-off refrigerators, stoves, washers, dryers (stuff unattached) in the first year. Think of it this way: you can upgrade your rental property, charge more rent, and reduce your taxable income.

Depreciation can get you into a lower tax bracket

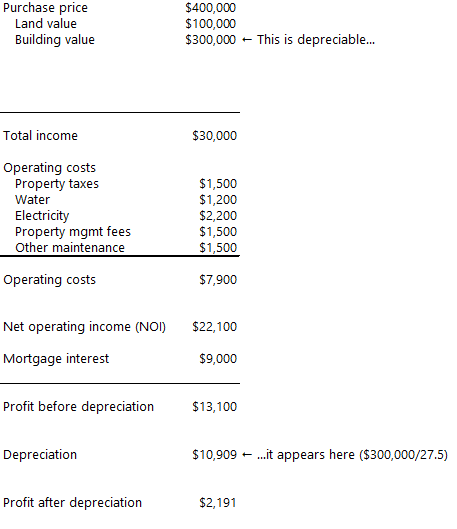

You can write-off the building portion of your investment over 27.5 years. Not the land.

Say you buy a place for $400,000 and rent it out. And say the land is valued at $100,000 (from the appraisal). That means the building value is $300,000 ($400,000 less $100,000). Every full year you own the property you can reduce your taxable income by $300,000/27.5 = $10,909. If you're in a higher Federal tax bracket, say 32%, that's a meaningful saving of $10,909 x 32% = $3,491. You might even get yourself into a lower tax bracket.

In this example the property's profit (NOI less mortgage interest) is $13,100.

But you don't get taxed on that profit.

You get taxed on the profit after depreciating the building value. So you would be taxed on $2,191. That's a much smaller amount than the $13,100 of real profit you made.

There are lots of asterisks on depreciation:

- When you sell the property, the depreciated amount is taxed at 25% (but even this you can avoid with a 1031 exchange, see below)

- If you're depreciation is more than your rental income, you can't carry forward losses (with some exceptions)

- Commercial real estate depreciates more slowly over 39 years

Get a tax-free lump of money if you refinance

You've owned a property for a few years and it's gone up in value. If you refinance you can 'cash out' some of the equity you've built up. You basically reset your mortgage at a higher amount.

That 'cash out' money is not taxable.

There are downsides to think through. Increased debt. The hassle of refinancing. But ultimately you've got tax-free money in your bank (to make another investment?).

Avoid, minimize or delay paying capital gains

If you don't sell, you don't have capital gains. Simple. But there are other smart (legal) ways to avoid, minimize or delay capital gains:

- MINIMIZE: Hold your property for more than a year (don't be a flipper) to avoid short-term capital gains.

- AVOID: Live in your investment property for 2 out of 5 years and make up to $500,000 (as a couple, $250,000 as a single person) tax-free.

- DELAY: 'Swap' your current investment for a like investment using a 1031 exchange (so called because of the IRS tax code). There are conditions attached: the property must be similar and of equal or greater value; you need a qualified intermediary; there's a time restriction to complete the transaction; furniture/appliances are exempt etc. But you get to defer capital gains from selling your property while trading up.

- AVOID: Die and leave your property to someone else. They don't get your tax burden. The first few million (!) are exempt from inheritance tax. And you never paid your capital gains. But on the negative side you didn't enjoy the capital appreciation and you're dead. Both bummers.

There are even more tax benefits not covered here like installment sales income, self-directed IRA investing, and opportunity zones. Consider those the advanced course.

Rental income has no payroll tax

If like me (and other lazy landlords) you have a salaried job, you'll have noticed a FICA (Social Security and Medicare tax) of 7.65%. You can't get around this (with some very specific exemptions).

The good news is that rental income has 0% FICA tax. I like 0% tax.

I'm no tax expert and I encourage you to get the independent and up-to-date tax advice (legal disclosure elsewhere). Rental tax policy is a moving target. That's why you shouldn't invest in real estate just because of the tax code. I pay an accountant so I stay on the right side of the IRS. It's just me being the Laziest Landlord possible.

To round out the analogy: there's a lot to digest with the tax advantages of real estate. But that's what happens when you get a free dessert with your dinner.

If you want all the tax details, read the IRS guidelines. It's reassuringly and unsurprisingly long.