Everyone uses this metric...I refuse to

Internal Rate of Return (IRR) is a common metric in real estate. Google "Real Estate" and "IRR". You'll see.

What is IRR? And why do I reject it? Let's start with the first. And then I'll explain why I would need psychic powers to not reject it.

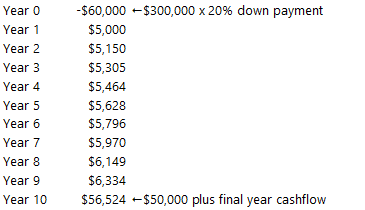

IRR is an all-in-one measure of future cash flows. It's loved in real estate because it is one number. (Easy to understand). It looks at cash flow. (Good). It's the interest earned on a dollar invested up front. It's best illustrated with an example.

Say I buy a property for $300,000 with 20% down. I do a quick P&L and figure out I'll generate $5,000 in cash flow for 10 years. I estimate this will increase 3% each year. And then I'll sell the property and gain $50,000 equity.

My IRR, Excel says, is 8.2%.

Here's why I reject IRR. I've had to make many assumptions. Big ones. Without being a psychic, I've had to assume:

- I will sell in 10 years' time.

- The value of the property a decade from now.

- Tax rates and depreciation write off to figure out annual cash flow.

- One off expenses and when they may (or may not) happen.

- Cash flow will continue increasing at a fixed percentage.

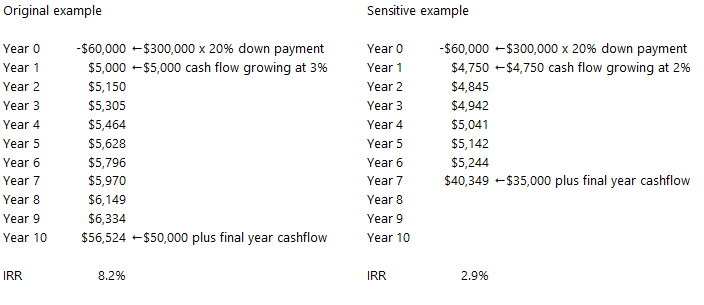

IRR is particularly sensitive to #1 and #2 above.

Let's take a very real possibility. The cash flow isn't $5,000 per year growing at 3% but $4,750 at 2%. And say I have to sell 7 years from now and not 10 and get $35,000 in equity rather than $50,000.

Suddenly my IRR no longer looks like a healthy 8.2%. It's now just 2.9%! And all I did was to tweak my assumptions slightly:

I get asked regularly "what's the IRR?" by people trying to sound smart. I reply "I don't care". Why? For the exact reason above. It's too sensitive to highly likely scenarios.

I look at five other metrics for the first five years. Why? Because they rely less (not zero) on assumptions. And they tell me useful things within a margin of error.

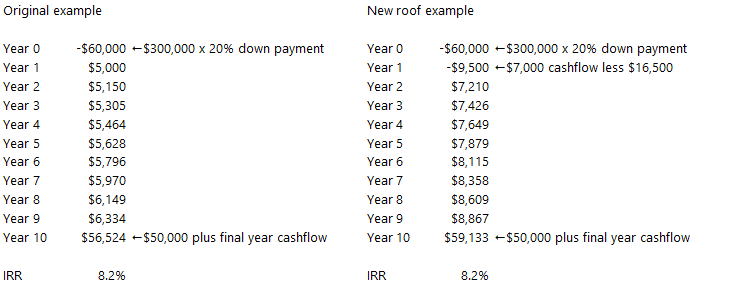

Here is another reason why I reject IRR. Say the same property is run down and requires $16,500 investment in a new roof. With a new roof I think I can get $7,000 a year in cash flow, again increasing by 3%.

Both have the same IRR. Which is better? I now have to put more cash in (do I have enough?) and hope I get more cash flow. But will my selling price be higher with a new roof 10 years from now?

Being the Laziest Landlord is about financial security. Security means a high degree of certainty. And IRR just doesn't have that certainty. It requires too many assumptions or great psychic powers.